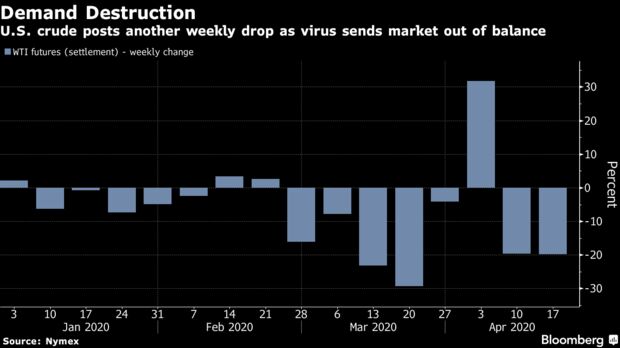

Oil extended its slide, falling to the lowest in more than two decades, on concern the world is rapidly running out of places to store crude after output cuts proved insufficient to cope with plunging demand.

Futures in New York fell 16% to around $15 a barrel after losing almost a fifth of their value last week as the deal by OPEC+ and other producers failed to counter the loss of demand from a crippled global economy. The current May contract expires Tuesday, however, with the more active June futures only down by less than half as much.

Near-term prices for West Texas Intermediate, the U.S. benchmark, are trading at huge discounts to later-dated contracts on concern the storage hub of Cushing, Oklahoma, will fill to capacity. That has seen prices disconnect from Brent futures in London. Buyers in Texas are offering as little as $2 a barrel for some oil streams, raising the possibility that American producers may soon have to pay customers to take crude off their hands.

The 9.7 million barrels a day of production cuts agreed by OPEC+ are paling in comparison against this backdrop. China reported its first economic contraction in decades on Friday, an indicator of what’s to come in Europe and North America, which have yet to emerge from coronavirus-driven lockdowns. There were some signs of optimism, however, as death rates eased in New York and some of the hardest-hit European countries.

“The current prices show that the OPEC+ cuts proved to be a blip, with oil prices at the mercy of the virus once again,” said Vandana Hari, founder of Vanda Insights in Singapore. “Until we approach a lifting of the lockdowns in the U.S,, oil may drift lower or remain rangebound around current levels.”

WTI for May delivery fell 16% to $15.37 a barrel on the New York Mercantile Exchange as of 9:16 a.m. in Singapore after plummeting 20% last week. It dropped to as low as $14.47, the weakest since March 1999. The June contact declined 6.4% to $23.42.

Brent for June delivery fell 1.6% to $27.63 a barrel on the ICE Futures Europe exchange after losing 10.8% last week.

“Concern continues to mount that storage facilities in the U.S. will run out of capacity,” with stockpiles at Cushing rising almost 50% since the start of March, Australia & New Zealand Banking Group Ltd. said in a note. “We hold some hope for a recovery later this year.”

The price collapse is reverberating across the oil industry. Crude explorers shut down 13% of the U.S. drilling fleet last week as the swelling worldwide glut of crude spurred drastic cost-cutting and project cancellations among drillers.